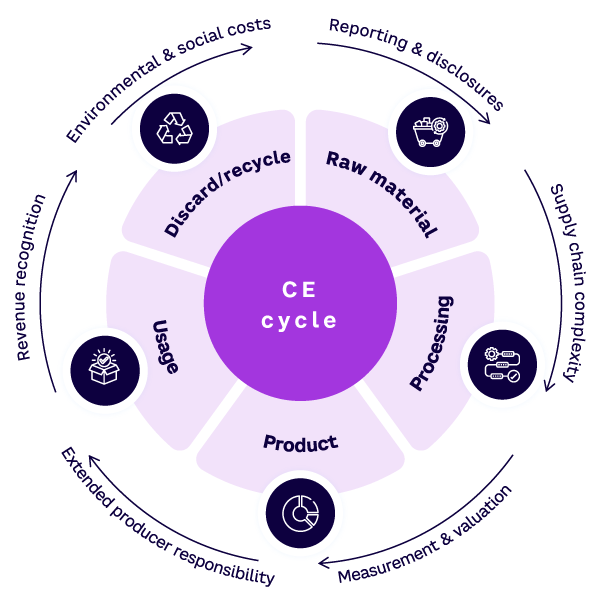

Let’s be honest. The old accounting playbook—the one built for a world of “make, sell, forget”—is starting to fray at the seams. It’s just not built for a world where a company retains ownership of a product for its entire life, or where waste is designed out of the system entirely. That’s the shift we’re seeing with the circular economy and its powerful engine, the Product-as-a-Service (PaaS) model.

For finance teams, this isn’t just a sustainability trend. It’s a fundamental rewire of revenue streams, asset management, and cost recognition. The numbers tell a different story now. And if your accounting practices don’t adapt, you risk misstating your financial health, confusing investors, and frankly, missing the strategic point of going circular in the first place.

Why Traditional Accounting Stumbles Here

Think of traditional accounting as a sprinter. It’s great for recognizing a quick sale—a burst of revenue, a clear cost of goods sold, done. The circular PaaS model, though? It’s a marathon runner. Revenue trickles in over years, and the asset (the physical product) keeps coming back for maintenance, refurbishment, and reuse.

The core tension is ownership. In a sale, you transfer risks and rewards. In a service model, you keep them. This flips key accounting concepts on their head:

- Revenue Recognition: That big upfront payment from a customer? It’s not revenue. It’s a liability—a deferred revenue obligation to provide service over time.

- Asset Capitalization: The products you lease out remain on your balance sheet as assets. Their value isn’t gone; it’s just… circulating.

- Cost Tracking: Repair, logistics, refurbishment—these aren’t peripheral expenses anymore. They’re core to delivering the service and are directly tied to the performance obligation.

So, the first best practice is a mindset shift: from accounting for products to accounting for performance and utility.

Building Your Circular Accounting Framework

1. Master the Art of Asset Lifecycle Tracking

This is the bedrock. Every single product in your service fleet needs a digital twin in your books. You’re not just tracking a laptop; you’re tracking Serial #XYZ through its initial lease, its return, its component harvest, its refurbishment, and its next lease cycle.

This requires robust fixed asset sub-ledgers. You’ll need to depreciate the asset not over its “useful life to oblivion,” but over its economic useful life within your circular system. That might be longer than you think, thanks to refurbishment. The depreciation schedule becomes a dynamic map of value retention.

2. Reframe Your P&L: Cost of Revenue Reimagined

Forget COGS. Welcome to the era of Cost of Revenue (COR) or Cost to Serve. This is where you capture the true cost of delivering the service promise. It should include:

- Direct labor for maintenance & repair

- Parts and materials for refurbishment

- Reverse logistics (getting the product back!)

- Quality assurance and testing

Accurately allocating these costs is crucial for pricing your service contracts profitably. If you don’t know what it truly costs to maintain an asset for 10 years, you’re flying blind.

3. Navigate Revenue Recognition (ASC 606 / IFRS 15)

This is the big one, and honestly, it often requires a chat with your auditor. Under the standards, you identify the performance obligation in the contract. In a pure PaaS model, it’s typically the continuous access to and performance of the product over the contract term.

You then allocate the transaction price (the total contract value) to that obligation and recognize revenue as you satisfy it—usually straight-line over the term. Here’s a simplified view:

| Action | Impact on Financials |

| Sign a 3-year PaaS contract for $30,000 | Cash: +$30,000 Balance Sheet: +$30,000 Deferred Revenue Liability |

| Recognize revenue monthly | P&L: +$833 Revenue each month Balance Sheet: Deferred Revenue decreases by $833 |

| Incur monthly service costs | P&L: Record under Cost of Revenue |

The Hidden Challenges (And How to Tackle Them)

Sure, the theory sounds clean. But the day-to-day gets messy. Here are a couple of the real-world headaches and how to think about them.

Valuing Recovered Materials & Components

When you take a product back and harvest a perfectly good motor or circuit board, what’s it worth? It’s not “free inventory.” Best practice is to value these components at their net realizable value—essentially, what you’d sell them for, or what you save by not buying them new. This creates a credit against your refurbishment costs, making the circular model’s economics crystal clear.

Managing Residual Value Risk

This is a big one. What if technology changes and your leased asset becomes obsolete faster than you depreciated it? You need to model and provision for this residual value risk. It’s an ongoing assessment—a bit like forecasting, but for your balance sheet’s asset values. Some companies even use separate asset pools for different product vintages.

Tech Stack Considerations: You Can’t Do This on Spreadsheets

Seriously, don’t try. The data granularity needed is immense. Look for systems that talk to each other:

- IoT & Asset Tracking: For real-time product location and condition data.

- ERP with Robust Fixed Asset & Service Management: The core ledger for lifecycle tracking.

- Subscription Billing Platforms: To handle the recurring invoicing and revenue scheduling aligned with ASC 606/IFRS 15.

Integration is key. The goal is a single source of truth for every physical product’s financial and physical journey.

The Bigger Picture: Accounting as a Strategic Compass

Here’s the thing—when you get this right, your financials stop being just a historical record. They become a strategic tool. You can see which product designs are cheaper to maintain. You can prove that refurbishment is more profitable than new manufacturing. You can show investors the value of your long-term, sticky customer relationships and your resilient asset base.

In a linear world, accounting looks backward. In a circular one, done well, it helps you steer forward. It quantifies the loop. And that, in the end, is the ultimate best practice: using the language of business—the balance sheet, the P&L—to tell the true story of a business that’s built to last, and built to regenerate.